Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Disability Income Mortgage Reports Quote

If you’re wondering if buying a home with disability income is possible, the good news is, the answer is yes.

If you want to learn more or explore your options for a home loan, connect with a lender. With the right team in place, we can make your dream of homeownership a reality.

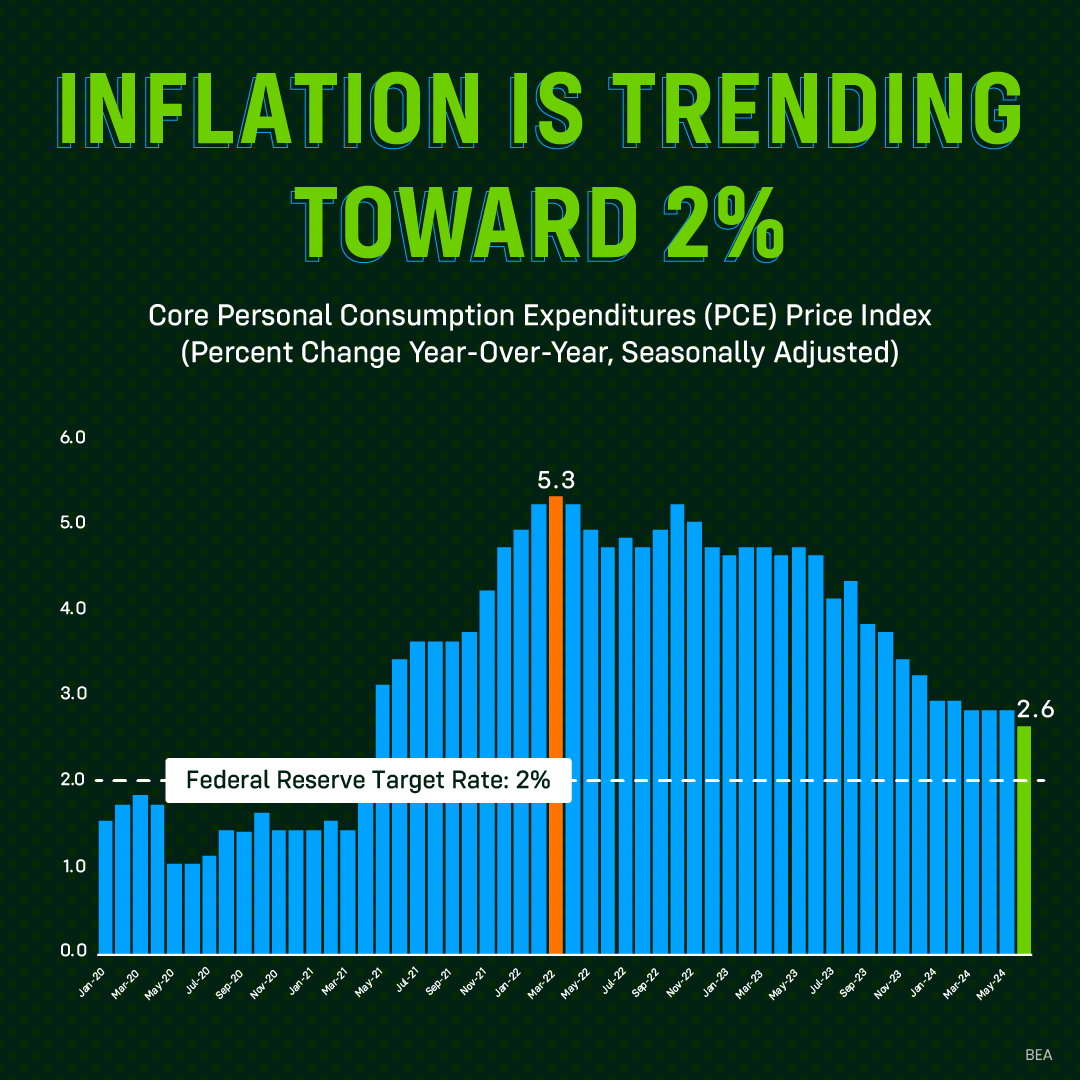

Inflation Is Trending Down

Inflation is cooling – and that’s a good sign for mortgage rates.

Once the rate of inflation reaches the Fed’s target of 2%, they may lower the Federal Funds Rate. When they do, mortgage rates are likely to respond.

But this isn’t the only factor at play. For the latest updates on what’s happening, follow me.

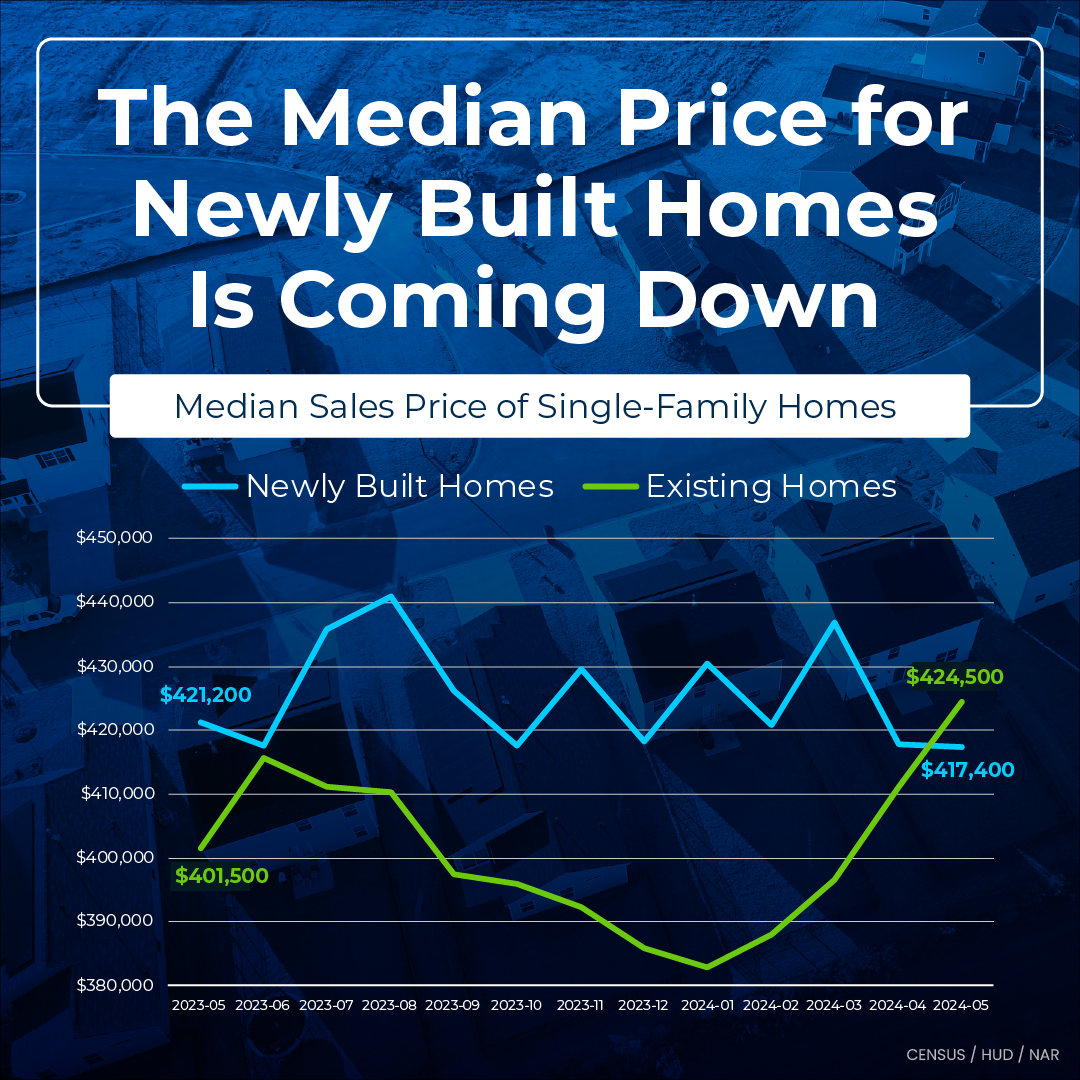

A Newly Built Home May Be More Cost-Effective

New trend alert.

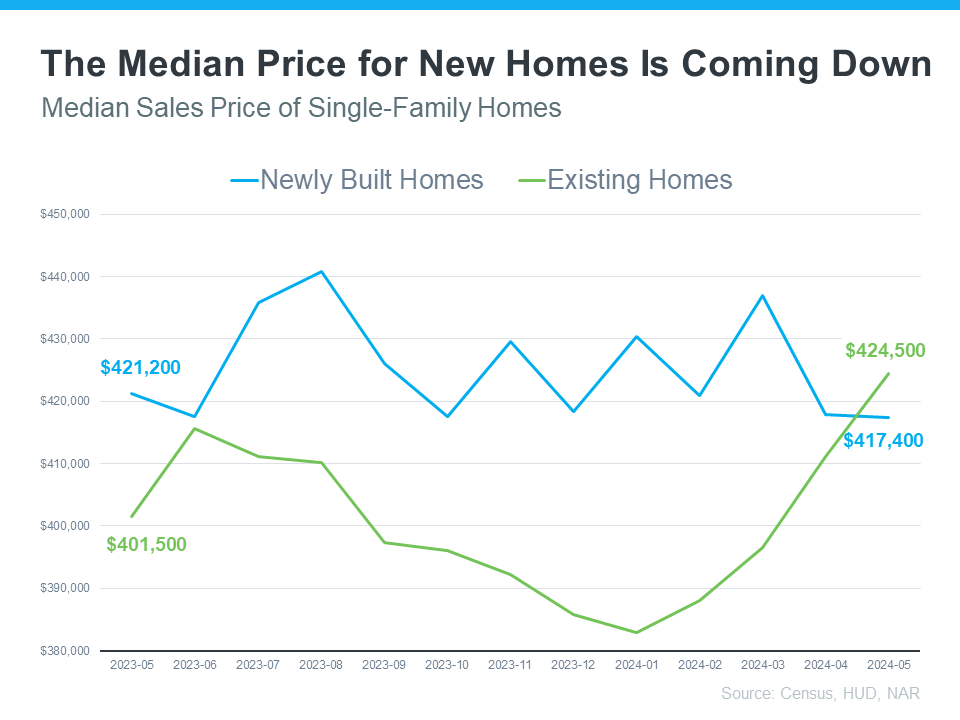

The median price for new builds has dipped lower than the median for existing homes.

Plus, some builders are tossing in sweet perks like competitive mortgage rates and free upgrades.

So, if you aren’t already considering brand-new homes, it may be worth looking into. Drop a comment with your dream home feature, and let’s find your perfect fit together.

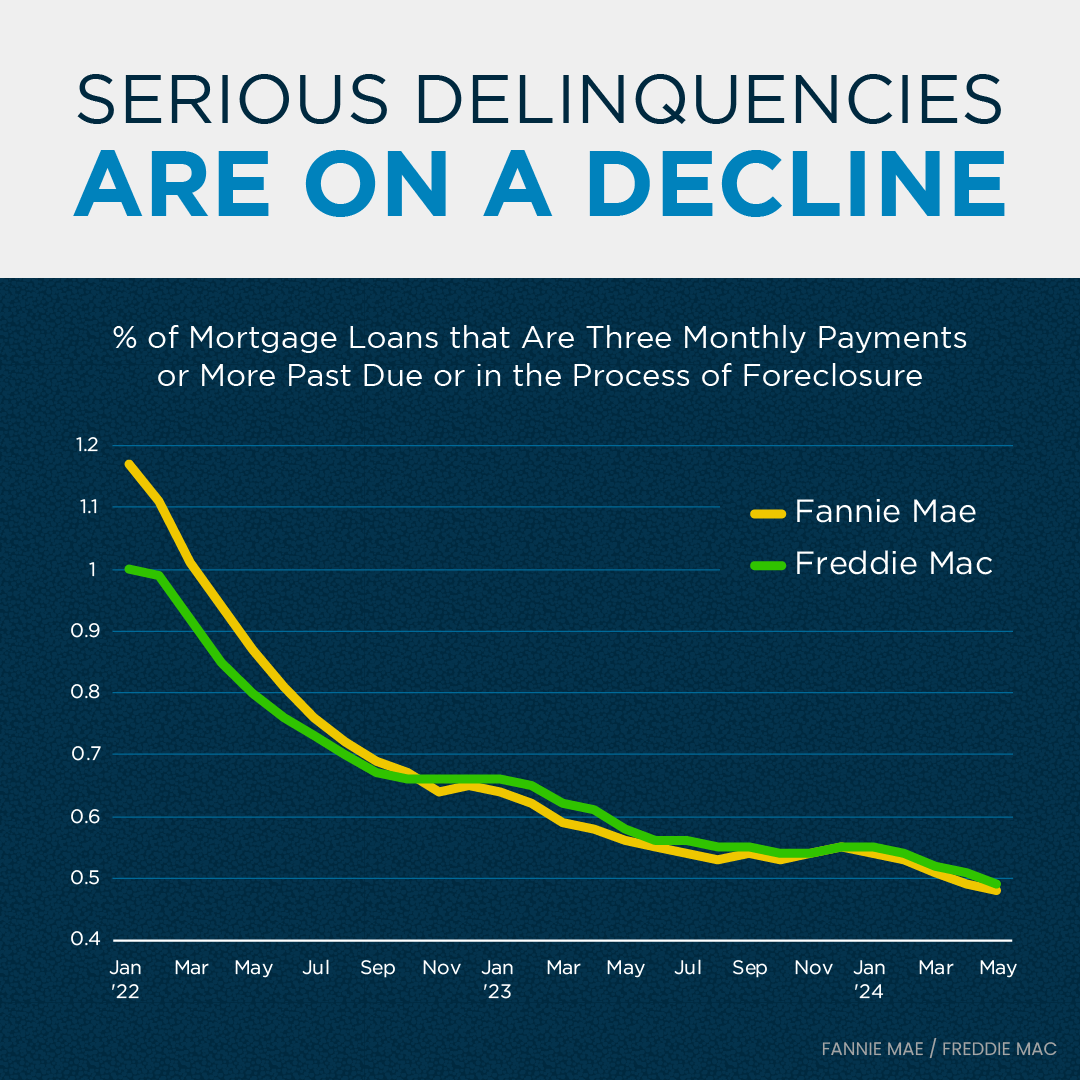

Foreclosure Delinquency Rates Are on the Decline

Do high prices at the gas pump and grocery store have you worried more people are going to fall behind on their mortgage payments?

If you’re thinking that’ll lead to a surge of foreclosures, let this reassure you.

Serious delinquencies (loans that are 3 or more monthly payments past due) are on the decline – so there’s no wave of foreclosures on the horizon.

Affordability Is Reshaping Migration Trends

Having a hard time finding a place to call home in your budget?

Thousands of Americans are on the move in search of better affordability.

That’s because broadening where you’re looking could help you find somewhere your money takes you a little further.

A Newly Built Home May Actually Be More Budget-Friendly

If you’re in the market to buy a home, there’s some exciting news for you. Many people assume that newly built homes are more expensive than existing ones (houses that have already been lived in), but that’s not always the case. In fact, exploring newly built homes can sometimes lead to more cost-effective options, especially today. Hard to believe, right? But the data doesn’t lie.

Here are two key reasons working with your agent to look into new home construction could help you find a more budget-friendly option.

Reason 1: Lower Median Prices for Newly Built Homes

The median sales price for newly built homes is lower than the median sales price for existing homes today. This might seem surprising, but it’s true according to the latest data from the Census and the National Association of Realtors (NAR):

Why is that? Builders are focused on building what they can sell. And right now, there’s a very real need for smaller and more affordable homes – so that’s what they’ve been bringing to the market. At the same time, there are also more newly built homes already on the market than there have been over the past few years, so builders are motivated to make sure they’re selling what they’ve got available before adding more.

Reason 2: Attractive Incentives from Home Builders

Another big reason to consider a newly built home is the range of incentives that many home builders are offering. Again, since builders are aiming to sell their current inventory, some are providing special deals to sweeten the pot for homebuyers. HousingWire explains today’s trend:

“Overall, the usage of sales incentives was up to 61% in June, compared to 59% in May.”

One of the most appealing incentives right now is how builders are able to offer competitive mortgage rates. They may also provide other incentives, such as covering closing costs, or offering free upgrades.

Why This Matters to You

Considering a newly built home could open up opportunities you hadn’t thought of before. With competitive pricing and attractive incentives, you might just find that a brand-new home is the most appealing option for you.

Bottom Line

Buying a home is a big decision, and it’s essential to consider all your options. By looking into newly built homes, you might find a perfect fit for your needs and your budget.

Let’s explore the possibilities together. If you have any questions or want to see what’s available, feel free to reach out.

Why a Foreclosure Wave Isn’t on the Horizon

Even though data shows inflation is cooling, a lot of people are still feeling the pinch on their wallets. And those high costs on everything from gas to groceries are fueling unnecessary concerns that more people are going to have trouble making their mortgage payments. But, does that mean there’s a big wave of foreclosures coming?

Here’s a look at why the data and the experts say that’s not going to happen.

There Aren’t Many Homeowners Who Are Seriously Behind on Their Mortgages

One of the main reasons there were so many foreclosures during the last housing crash was because relaxed lending standards made it easy for people to take out mortgages, even when they couldn’t show they’d be able to pay them back. At that time, lenders weren’t being as strict when looking at applicant credit scores, income levels, employment status, and debt-to-income ratio.

But since then, lending standards have gotten a whole lot tighter. Lenders became much more diligent when assessing applicants for home loans. And that means we’re seeing more qualified buyers who have less of a risk of defaulting on their loans.

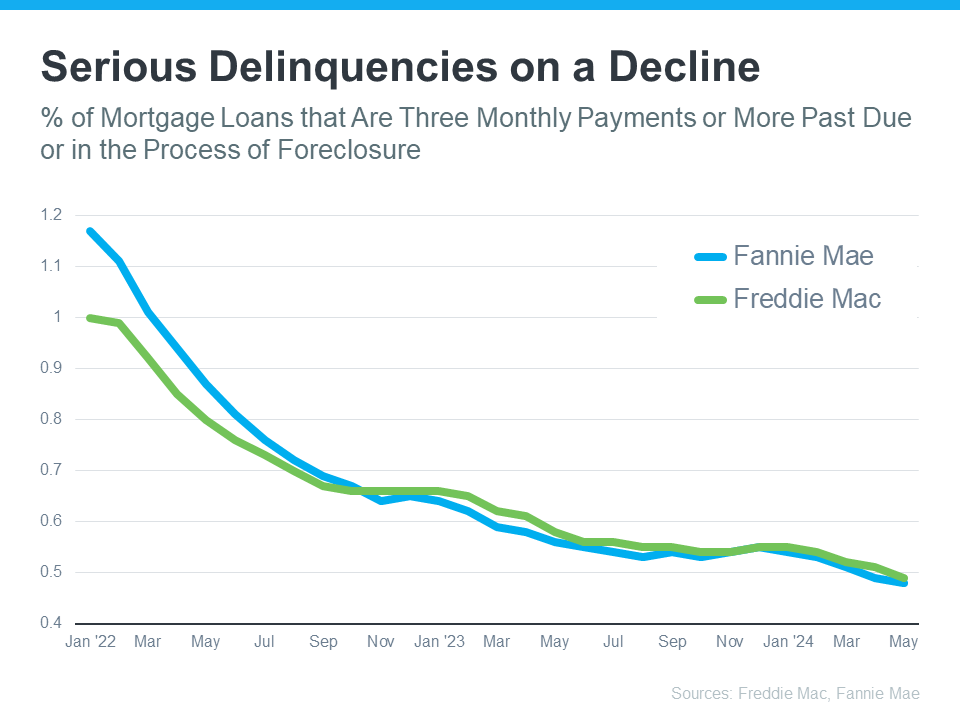

That’s why data from Freddie Mac and Fannie Mae shows the number of homeowners who are seriously behind on their mortgage payments (known in the industry as delinquencies) has been declining for quite some time. Take a look at the graph below:

What this means is that, not only are borrowers more qualified, but they’re also finding ways to navigate through their challenges, exploring their repayment options, or maybe even using the record amount of equity they have to sell and avoid foreclosure entirely.

The Answer Is: There’s No Sign of a Wave Coming

Before there can be a significant rise in foreclosures, the number of people who can’t make their mortgage payments would need to rise significantly. But, since so many buyers are making their payments today and homeowners have so much equity built up, a wave of foreclosures isn’t likely.

Take it from Bill McBride of Calculated Risk – an expert on the housing market who, after closely following the data and market leading up to the crash, was able to see the foreclosure crisis coming in 2008. McBride says:

“We will NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble) for two key reasons: 1) mortgage lending has been solid, and 2) most homeowners have substantial equity in their homes.”

Bottom Line

If you’re worried about a potential foreclosure crisis, know there’s nothing in the data to suggest that’ll happen. Buyers are more qualified now, and that’s one reason why they’re not falling seriously behind on their mortgage payments.